accumulated earnings tax c corporation

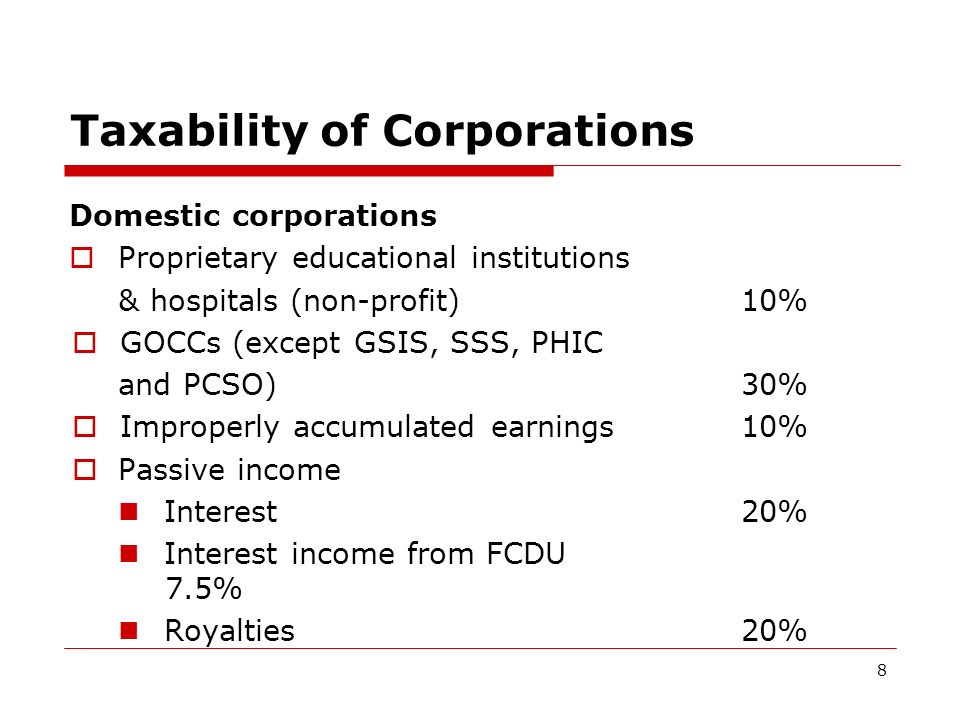

Accumulated Earnings Tax The AET is a 20 percent tax for each tax year on accumulated taxable income of corporations1 While the AET hasnt been widely imposed or litigated in recent years it still applies to all corporations with limited exceptions2 formed or used to avoid the individual income tax. The threshold is 25000 without accumulated earning tax.

Demystifying Irc Section 965 Math The Cpa Journal

Corporations formerly registered with PEZA c.

. He accumulated earnings tax AET is imposed by Internal Revenue Code IRC section 531 on C corporations formed or availed of for the purpose of avoiding the imposi-tion of income tax on their shareholders by permitting earnings and profits to be accumulated instead of being distrib-uted. Our Easy Step-By-Step Process Takes The Guesswork Out Of Filing Self-Employed Taxes. Tax Notes -Now I Am a C Corp.

Accumulated earnings can be reduced by dividends actually or deemed paid and corporations are entitled to an accumulated earnings credit which will be the greater of 1 a minimum of a 250000. The AET is a penalty tax imposed on corporations for unreasonably accumulating earnings. The tax rate on accumulated earnings is 20 the maximum rate at which they would be taxed if distributed.

As the difference between ordinary income tax rates and capital gains tax rates increases corporations have sought to minimize dividend payments to shareholders with the objective of helping them secure capital gains taxed at a lower rate. EP generated in a C corporation are subject to two levels of taxation corporate and shareholder and retain this character even if subsequently owned by an S corporation. Accumulated EP was taxed at the C corporation level and will be taxed again as a dividend to recipient S corporation shareholders when distributed.

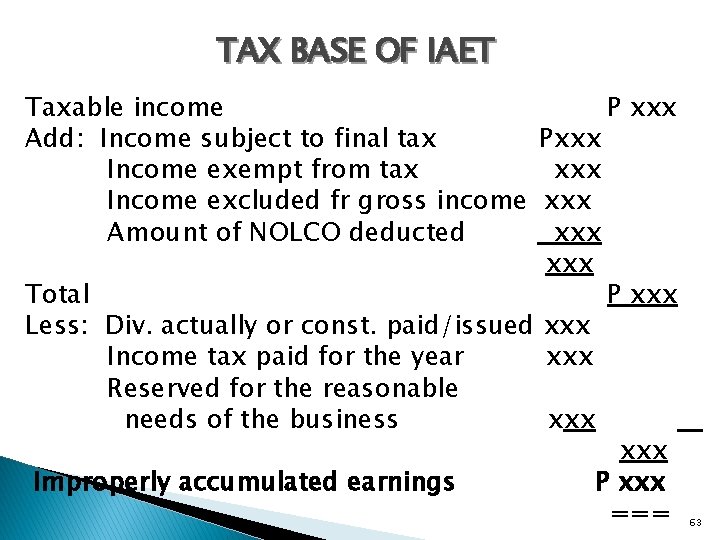

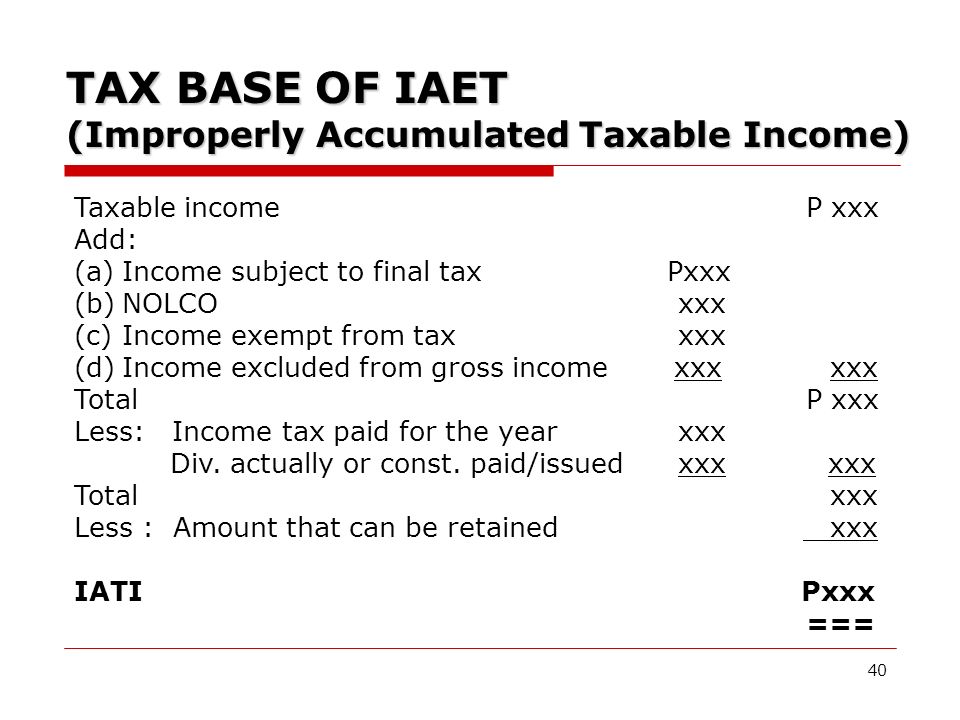

The IRS also allows certain exemptions based on the required. Accumulated taxable income is the corporations taxable income with certain adjustments and minus the sum of the dividends-paid deduction 259 and the accumulated earnings credit 261. However if a corporation allows earnings to accumulate beyond the reasonable needs of the business it may be subject to.

Accumulated earnings and profits are a companys net profits after paying dividends to the. To prevent companies from doing this Congress adopted the excess accumulated earnings tax provision of IRC section 535. Haidia corporation an educational institution provided the following data for the current year.

Ad TurboTax Helps You File Self-Employed Taxes The Way You Want And With Confidence. The accumulated earnings tax is an annual tax levied on modified taxable income Sec. This is because corporations that do not spend retained earnings are.

The tax is in addition to the regular corporate income tax and is assessed by the IRS typically during an IRS audit. Income from tuition fees P3500000 School. The accumulated earnings tax imposed by section 531 shall apply to every corporation other than those described in subsection b formed or availed of for the purpose of avoiding the income tax with respect to its shareholders or the shareholders of any other corporation by permitting earnings and profits to accumulate instead of being divided or distributed.

According to the IRS anything. As a practical matter the tax is col-. The federal government discourages companies from stockpiling their capital by using the accumulated earnings tax.

Under current tax law an S corporation cannot produce earnings and profits EP. Any corporation within a chain of corporations can be subject to the accumulated earnings tax. A corporation can accumulate its earnings for a possible expansion or other bona fide business reasons.

The accumulated earnings tax 251 is imposed on a corporations accumulated taxable income for the tax year. Bank and Non-bank Financial Intermediaries 79. May 17th 2021.

Publicly held corporations d. Typical C corporations where shareholders are taxed separately from the company may retain up to 250000 of their earnings before. Accumulated earnings and profits EP is an accounting term applicable to stockholders of corporations.

The improperly accumulated earnings tax shall not apply to the following except. There is a certain level in which the number of earnings of C corporations can get. When the revenues or profits are above this level the firm will be subjected to accumulated earnings tax if they do not distribute the dividends to shareholders.

Private and publicly held corporations are subject to this tax but it does not impact passive foreign investment companies tax-exempt organizations and personal holding companies. Breaking Down Accumulated Earnings Tax. This gives very little leeway for C corporations to pay the 21 tax and build up savings without dividends unless there are provable business needs to accumulate more.

The accumulated earnings tax rate is 20. The accumulated earnings tax is computed on the corporations accumulated taxable income for. For C corporations the current accumulated retained earnings threshold that triggers this tax is 250000.

Exemption levels in the amounts of 250000 and 150000 depending on the company exist. 535b retained in the business in excess of its reasonable needs. This taxadded as a penalty to a companys income tax liabilityspecifically applies to the companys taxable income less the deduction for dividends paid and a standard accumulated tax credit of 250000 150000 for personal service.

A subsidiary corporation can be subject to the accumulated earnings tax even though the parent corporation is not subject to the accumulated earnings tax and vice versa. Our system imposes a 20 percent tax on accumulated taxable income of a corporation availed of to avoid tax to shareholders by permitting earnings and profits to accumulate rather than being paid out. Posted on Wednesday May 15 2019 In this article Cory Stigile provides background on the accumulated earnings tax and explains the steps corporate taxpayers may be able to take if the government begins to more.

What About the Accumulated Earnings Tax. By CORY STIGILE Posted by Hochman Salkin Toscher Perez PC. S corporations that have accumulated.

However if the S corporation itself was previously a C corporation it may have accumulated EP from years when it was a C corporation.

What Are Accumulated Earnings Definition Meaning Example

Earnings And Profits Computation Case Study

Understanding The Accumulated Earnings Tax Before Switching To A C Corporation In 2019

Income Tax Computation For Corporate Taxpayers Prepared By

Earnings And Profits Computation Case Study

Determining The Taxability Of S Corporation Distributions Part Ii

Corporate Distributions

Owners Equity Net Worth And Balance Sheet Book Value Explained

Income Tax Computation Corporate Taxpayer 1 2 What Is A Corporation Corporation Is An Artificial Being Created By Law Having The Rights Of Succession Ppt Download

Determining The Taxability Of S Corporation Distributions Part Ii

Corporate Accumulation Penalty Taxes

Overview Of Improperly Accumulated Earnings Tax In The Philippines Tax And Accounting Center Inc Tax And Accounting Center Inc

2

Oh How The Tables May Turn C To S Conversion Considerations Stout

S Corp Rias Disadvantaged By The Tax Bill Mercer Capital

How To Calculate The Accumulated Earnings Tax For Corporations Universal Cpa Review

Oh How The Tables May Turn C To S Conversion Considerations Stout

Determining The Taxability Of S Corporation Distributions Part I

Income Tax Computation Corporate Taxpayer 1 2 What Is A Corporation Corporation Is An Artificial Being Created By Law Having The Rights Of Succession Ppt Download